A Brinks armored truck sits parked in front of the shuttered Silicon Valley Bank (SVB) headquarters on March 10, 2023 in Santa Clara, California.

Justin Sullivan | Getty Images

On Wednesday, Silicon Valley Bank was a well-capitalized institution searching for to lift some capital.

Inside 48 hours, a panic induced by the very enterprise capital community that SVB had served and nurtured ended the bank’s 40-year-run.

Regulators shuttered SVB Friday and seized its deposits in the biggest U.S. banking failure because the 2008 financial crisis and the second-largest ever. The corporate’s downward spiral began late Wednesday, when it surprised investors with news that it needed to lift $2.25 billion to shore up its balance sheet. What followed was the rapid collapse of a highly-respected bank that had grown alongside its technology clients.

Even now, because the dust begins to decide on the second bank wind-down announced this week, members of the VC community are lamenting the role that other investors played in SVB’s demise.

“This was a hysteria-induced bank run attributable to VCs,” Ryan Falvey, a fintech investor at Restive Ventures, told CNBC. “That is going to go down as one among the final word cases of an industry cutting its nose off to spite its face.”

The episode is the newest fallout from the Federal Reserve’s actions to stem inflation with its most aggressive rate climbing campaign in 4 many years. The ramifications could possibly be far-reaching, with concerns that startups could also be unable to pay employees in coming days, enterprise investors may struggle to lift funds, and an already-battered sector could face a deeper malaise.

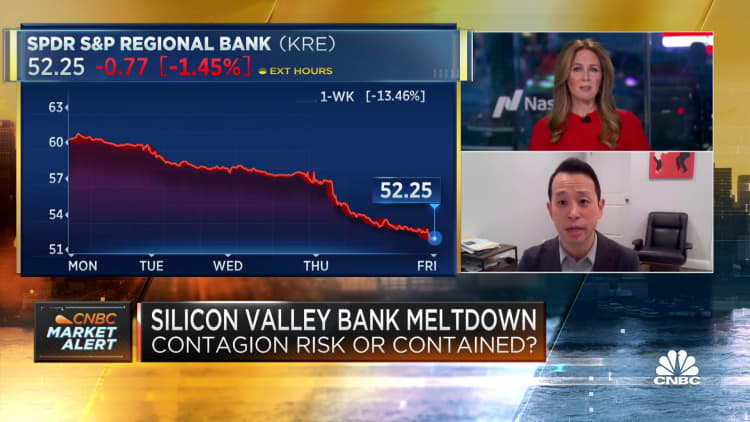

Shares of Silicon Valley Bank collapsed this week.

The roots of SVB’s collapse stem from dislocations spurred by higher rates. As startup clients withdrew deposits to maintain their firms afloat in a cold environment for IPOs and personal fundraising, SVB found itself short on capital. It had been forced to sell all of its available-for-sale bonds at a $1.8 billion loss, the bank said late Wednesday.

The sudden need for fresh capital, coming on the heels of the collapse of crypto-focused Silvergate bank, sparked one other wave of deposit withdrawals Thursday as VCs instructed their portfolio firms to maneuver funds, in accordance with individuals with knowledge of the matter. The priority: a bank run at SVB could pose an existential threat to startups who couldn’t tap their deposits.

SVB customers said CEO Greg Becker didn’t instill confidence when he urged them to “stay calm” during a call that began Thursday afternoon. The stock’s collapse continued unabated, reaching 60% by the top of standard trading. Importantly, Becker couldn’t assure listeners that the capital raise could be the bank’s last, said an individual on the decision.

Death blow

All told, customers withdrew a staggering $42 billion of deposits by the top of Thursday, in accordance with a California regulatory filing.

By the close of business that day, SVB had a negative money balance of $958 million, in accordance with the filing, and didn’t scrounge enough collateral from other sources, the regulator said.

Falvey, a former SVB worker who launched his own fund in 2018, pointed to the highly interconnected nature of the tech investing community as a key reason for the bank’s sudden demise.

Outstanding funds including Union Square Ventures and Coatue Management blasted emails to their entire rosters of startups in recent days, instructing them to tug funds out of SVB on concerns of a bank run. Social media only heightened the panic, he noted.

“While you say, `Hey, get your deposits out, this thing is gonna fail,’ that is like yelling fire in a crowded theater,” Falvey said. “It is a self-fulfilling prophecy.”

One other enterprise investor, TSVC partner Spencer Greene, also criticized investors who “were mistaken on the facts” about SVB’s position.

“It appears to me that there was no liquidity issue until a few VCs called it,” Greene said. “They were irresponsible, after which it became self-fulfilling.”

‘Business as usual’

Thursday evening, some SVB customers received emails assuring them that it was “business as usual” on the bank.

“I’m sure you’ve got been hearing some buzz about SVB within the markets today so wanted to achieve out to supply some context,” one SVB banker wrote to a client, in accordance with a duplicate of the message obtained by CNBC.

“It’s business as usual at SVB,” the banker wrote. “Understandably there could also be questions and I intend to make myself available if you might have any concerns.”

By Friday, as shares of SVB continued to sink, the bank ditched efforts to sell shares, CNBC’s David Faber reported. As an alternative, it was searching for a buyer, he reported. However the flight of deposits made the sale process harder, and that effort failed too, Faber said.

A customer stands outside of a shuttered Silicon Valley Bank (SVB) headquarters on March 10, 2023 in Santa Clara, California.

Justin Sullivan | Getty Images

Falvey, who began his profession at Wells Fargo and consulted for a bank that was seized in the course of the financial crisis, said that his evaluation of SVB’s mid-quarter update from Wednesday gave him confidence. The bank was well capitalized and will make all depositors whole, he said. He even counseled his portfolio firms to maintain their funds at SVB as rumors swirled.

Now, because of the bank run that led to SVB’s seizure, those that remained with SVB face an uncertain timeline for retrieving their money. While insured deposits are expected to be available as early as Monday, the lion’s share of deposits held by SVB were uninsured, and it’s unclear once they might be freed up.

“The precipitous deposit withdrawal has caused the Bank to be incapable of paying its obligations as they arrive due,” the California financial regulator stated. “The bank is now insolvent.”