NicoElNino

In our report titled Preparing for the 2020s dated August 3, 2022, we drew comparisons to the Twenties, arguing that initial enthusiasm for the post COVID-19 boom to resemble the Twenties was too premature. We showed that before the roaring Twenties commenced, the economy suffered a serious bout of inflation that was snuffed out by a deep recession in 1920-21. Upon economic recovery, the Twenties economy was then characterised by passive government, low inflation, and robust productivity.

Following the COVID-19 pandemic the economy is now experiencing the best inflation in forty years, and a monetary authority which is hell bent on snuffing it out via a decent credit policy. That is raising the chance of recession with some like us believing it’s already in progress and more likely to extend into 2023. Others consider the true recession is not going to hit until sometime in 2023. Regardless, the true issue is that when cyclical excesses are cleansed, is the economy of the 2020s able to exhibiting characteristics of the Twenties?

Our answer is a tentative affirmative depending on two phenomena. One is a return of a passive government. This we argue would take the shape of two-party rule, because the economy seems to have operated quite well over time under this manner. The more necessary condition for prosperity is a revival of productivity growth. That is crucial in holding down inflation, which in turn could be a springboard for faster economic growth.

The unique mandate of the Federal Reserve was to stop financial panics and bubbles. The present mandate is to realize maximum employment and price stability. On average the economy of the Twenties registered a 4% jobless rate, 5% real GDP growth, and an annualized decline of 1.5% in the patron price index. The equity market appreciated significantly and near the top of the last decade, to stop what it perceived as a bubble, the Federal Reserve doubled its’ discount rate. This was the prelude to the stock market crash in October 1929. Were the Fed to be fortunate enough to oversee such an economic backdrop within the 2020s, under its current mandate it might don’t have any reason to regulate monetary policy toward restraint.

Economic growth is primarily a function of the expansion of the labor force and the productivity of the labor force. Productivity is a key ingredient in achieving price stability. Within the Twenties productivity rose by an average 5.4% yearly within the manufacturing economy and a pair of.3% yearly in the general economy as shown on Table I attached. The economy was largely manufacturing based during that period and there was a relative reduction in the availability of labor. In the course of the first a part of the century the majority of paid work was performed by males. The flu pandemic of 1918-19 was particularly devastating for males, and it was mostly males who fought and died in World War I. The COVID-19 pandemic didn’t distinguish by gender. Females comprise a much larger segment of the labor force now, and so the relative supply of labor was similarly constrained. In 2019 the civilian labor force totaled 163.5 million and was growing 0.9% yearly. In 2020 the labor force declined by 1.75% and has yet to completely get well.

The slowing of labor force growth and participation is being accentuated by a protracted secular downtrend in the typical workweek. In the course of the industrial revolution a ten-hour seven day workweek was common. After the Civil War the Aldrich report estimated the workweek in manufacturing went from 69 hours in 1850 to 60 hours by 1890 and by 1910 it had fallen to 57.3 hours. Just prior to the onset of World War II the workweek averaged 37.6 hours.

This downtrend occurred in tandem with a decline in child labor. The Keating Owen Child Labor Act of 1916 banned children under age 14 from factory work. It was struck down by the Supreme Court, but by 1920 many states passed laws banning child labor. The Twenties was also a decade of reduced immigration. Over 1.0 million people immigrated to the U.S. annually prior to the primary World War. The war disrupted the inflow and in 1921 and 1924 laws imposed strict quotas on recent entrants.

If these restrictions had occurred in a vacuum, economic growth would have been sharply constrained. However the Twenties was a decade of great innovation which was prompted by electrification and the inner combustion engine. These impacted every sector of the economy and sharply boosted productivity. The 5.4% average annual rise in productivity over the course of the last decade was instrumental in the last decade’s record of noninflationary economic growth.

Like the start of the Twenties, the economy of the 2020s is facing constraints within the labor supply. As noted, COVID-19 has been a very important factor, restrictions on immigration are also playing a task. While illegal border crossings grab a great deal of headlines, there may be a broad consensus within the business community that restrictions on visas and legal processes are creating labor shortages. The flexibility of business to profit from low wage foreign labor also seems past its peak as deglobalization is starting to take hold in response to provide chain disruptions and political tensions.

China is a principal goal of western efforts to deglobalize. And yet China itself is facing a dwindling supply of low cost labor attributable to demographics and a growing preference amongst younger cohorts for service industry jobs versus manufacturing. As an offset, China is attempting to rapidly automate. The International Federation of Robotics estimates that shipments of commercial robots to China rose by 45% from the previous yr and accounted for roughly half of all installations of professional quality robots.

Deglobalization could be a two-edged sword if handled properly. On the one hand the substitution of low wage labor with high wage labor could possibly be inflationary. But a rising price of labor relative to capital could possibly be a spur to innovation and productivity, and thus find yourself being deflationary. Indeed, an August 2022 Wall Street Journal article ‘U.S. Firms on Pace to Bring Home Record Variety of Overseas Jobs’, addressed this topic. The article quoted Harry Moser, founder and president of Reshoring Initiative as saying corporations must automate to offset the upper cost of labor domestically. And in accordance with the Association for Advancing Automation, North American corporations ordered a record 11, 595 robots value $646 million in the primary quarter of this yr.

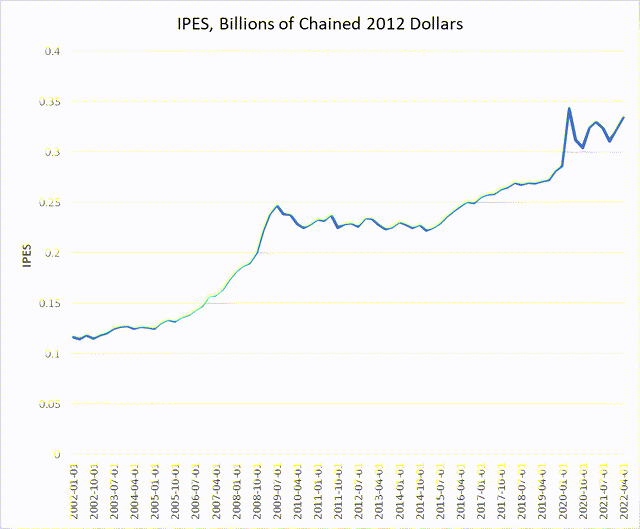

There isn’t any data series for robotic equipment activity. Nevertheless, included in the federal government national income accounts under gross private domestic investment (GPDI) is a category titled information processing equipment and software (IPES). The series seems representative of automation broadly defined. Data is quarterly starting in 2002 and is shown as Chart I attached. For perspective real GPDI rose by about 70% over the period while IPES spending rose by over 400%. Unlike GPDI which experienced dips, IPES was not negatively impacted by events just like the oil collapse of 2015-16 or the Boeing 737 Max crashes of 2018. However the pandemic induced economy meltdown showed a dip. While it is just not certain, our intuition is that IPES investment is benefiting from the accelerated depreciation provisions within the 2017 tax cut laws.

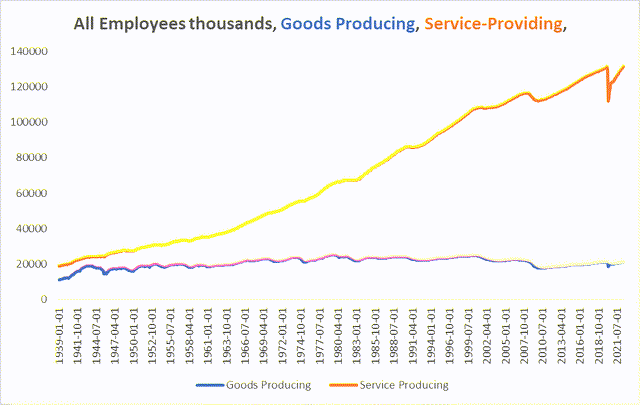

For the economy’s productivity rate to even remotely resemble the record of the Twenties, it’s going to should affect the service sector. Unlike that precedent days, the economy is significantly more tilted to the service sector. As shown on Chart II attached, the number of products producing employees has grown from about 11 million in 1939 to about 21 million currently. The variety of service industry employees has risen from about 19 million in 1937 to about 131 million currently. As this shift within the labor supply has occurred, the ultimate consumption of products versus services has not modified materially. Nominal goods consumption has risen about 7% yearly on average for the reason that end of World War II while service industry consumption has risen by barely greater than 7% yearly.

In fact, productivity is more exactly measured in the products sector since the comparison is between widgets and manhours. There isn’t any such comparison within the service sector. Thus, as service industry activity grew, manufacturing productivity easily outpaced the economy wide growth rate as shown on Table I. And as is clear from the table, the shift toward services has coincided with a downward drift in economy wide productivity growth over time.

Robots and automation could thus be very necessary in boosting the efficiency of the service sector and the complete economy. In fact, predicting the trail of productivity improvement is difficult, particularly since it is in regards to the future. Nevertheless, there may be a growing list of anecdotal evidence that’s encouraging. In late August CNBC published a report titled “Panera Bread tests artificial intelligence technology…” which noted that the corporate is using Open City’s voice-ordering technology that interacts with customers once they pull as much as the drive-thru speaker. McDonald’s can also be working to automate its drive-thru lane, announcing a partnership last yr with IBM to work toward that goal.

In late August a Latest York Times report noted that Blank Street Coffee has a business model using automation to take orders. Its stores would typically operate with only two employees per shift versus the nine employees per shift at a typical Starbucks.

Fast food establishments now have a serious incentive to adopt automation as California’s governor signed the Fast Food Accountability and Standards Recovery Act. It establishes a ten member Fast Food Sector Council that’s tasked with establishing standards on minimum wages, maximum working hours, training, and other working conditions applicable to industry employees. It is predicted to impose a $22 per hour minimum wage amongst other standards. The Society for Human Resource Management has warned that it will very likely speed up the usage of technological efficiencies and innovations in drive through ordering and kitchen equipment.

As an extra strike on the fast-food industry, in early September the Latest York Times reported that federal regulators have proposed a rule that will make more corporations legally answerable for labor law violations committed by their contractors and franchisees. Under the proposed rule which governs when an organization is taken into account a so-called joint employer, the National Labor Relations Board could hold an organization like McDonalds liable if one among its franchisees fired employees who tried to unionize, even when the parent company exercised only indirect control over the employees.

A potentially significant productivity improvement could result from the introduction of autonomous or self-driving vehicles. Before self-driving cars develop into a reality it is probably going that the technology will probably be deployed on business vehicles corresponding to trucks and delivery vans. These typically follow predetermined routes versus operating in several areas and road conditions. One self-driving truck could operate 24 hours per day, seven days per week and thus could replace 4 or 5 human drivers. A self-driving truck must be refueled, nevertheless it never takes a meal or rest break; it never gets sick; and it never goes on strike or takes a vacation.

Finally, nonetheless one views the recently enacted $50 billion CHIPS Act, it is for certain that consequently the availability of semiconductors will increase, especially since recipients of federal largess are expected to get additional funding from private and state and native sources. Not all semiconductors go into artificial intelligence technology processing equipment and software. But greater availability of semiconductors should lower research and development costs and hasten the advancement of recent and existing technological equipment.

There are some tentative conclusions that might be drawn from this historical sketch and the road ahead. First, we noted on the outset that a very important element of the Twenties boom was a passive government combined with a series of tax reductions and business friendly policy. In our previous report on Preparing for the 2020s we suggested that political gridlock could be the equivalent in the present period and merely making everlasting the 2017 tax reduction could be the equivalent of a tax cut.

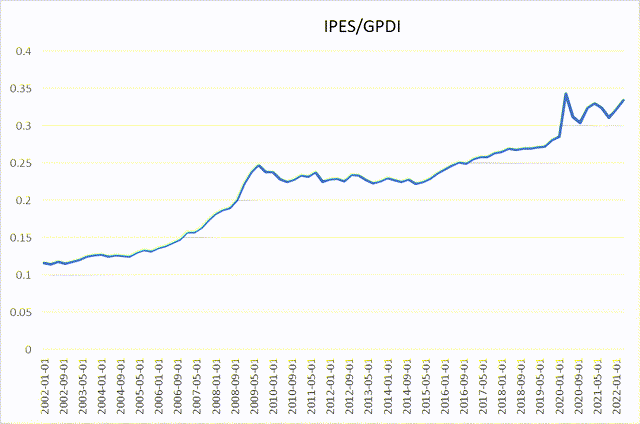

From the anecdotal reports we now have cited, one might conclude that the present direction is toward more lively government involvement within the private sector. Perhaps, but perversely a number of the barriers currently being erected would increase the inducement for affected businesses to take steps to limit their exposure. The result is probably going to scale back headcounts in affected industries but additionally to introduce recent efficiencies. Because of this, we’d expect spending on IPES to proceed increasing its share of overall GPDI as Chart III attached shows it has been doing. This we expect will show up in an improvement within the economy’s overall productivity growth rate. It can not match the torrid rate of the Twenties, but only a one percentage point increase within the economy’s abysmal productivity performance of the last ten years would get us back to the record of the Nineties. It is a formidable goal but not an unimaginable one by any means.

The Federal Reserve is working on the belief that the economy’s trend growth rate is barely below 2% annually. The Fed continually overestimated the magnitude of the recovery from the 2008-09 financial crisis. The Fed continually overestimated the inflation rate over the past ten years, and within the post pandemic period to this point the Fed has underestimated each growth and inflation. We expect this abysmal record stands probability of being repeated over the approaching ten years, especially if productivity growth recovers. Such an consequence could be a positive for all.

|

Table I Growth Rate Annual % Output/Hour for Chosen Periods |

|||

|

Manufacturing |

Private Nonfarm Economy |

||

|

1901-1919 |

1.71 |

||

|

1919-1929 |

5.45 |

2.27 |

|

|

1929-1941 |

2.61 |

2.35 |

|

|

1941-1948 |

0.2 |

1.71 |

|

|

1949-1973 |

2.51 |

2.88 |

|

|

1973-1989 |

2.42 |

1.34 |

|

|

1989-2000 |

3.56 |

1.92 |

|

|

2001-2010 |

3.57 |

2.39 |

|

|

2011-2019 |

-0.06 |

0.92 |

|

|

2011-2020 |

-0.58 |

1.07 |

|

|

2020-2021 |

1.18 |

1.86 |

|

Source: Prepared by Writer with data from BLS and Bureau of the Census

Chart I

Chart I IPES, Billions of Chained 2012 Dollars (BEA)

Chart II

All Employees 1000’s Goods Producing, Service-Providing (BLS)

Chart III

IPES as a share of GPDI (BEA) All Employees thousand Goods Producing, Service-Providing (BLS)

Please note that this text was written by Dr. Vincent J. Malanga and Dr. Lance Brofman with sponsorship by BEACH INVESTMENT COUNSEL, INC. and is used with the permission of each.