Bits and Splits_AdobeStock

COMMENTARY

*Editor’s note: All references in the primary person are references to the primary writer, Daven E. Morrison, III, MD, a board-certified psychiatrist.

As readers of Psychiatric Times™, you all are well educated and certain aware of the story of how, when asked why he stole from banks, Willie Sutton famously said, “Because that’s where the cash is.” It’s a clever quip, but unfortunately, it’s apocryphal. In his book Where the Money Was: The Memoirs of a Bank Robber (1976), Sutton denies having said this, but concedes that, “If anybody had asked me, I’d have probably said it.”1

Fraud traps people like that: It sounds too good not to be true. Barry Minkow of ZZZZ Best fraud notoriety observed that, “Fraud is the skin of truth filled with a lie.”2

Prior to now, we’ve got focused only on the overt economic consequences of fraud. It is obvious now that the covert “psychology of fraud” is an excellent more vital dimension we’d like with a purpose to truly understand fraud.

The way in which fraud entered my skilled life was quite dramatic. It eternally modified the arc of my profession as a psychiatrist. It’s fair to say that just as victims are seduced by fraudsters, as an organizational psychiatrist, I even have been seduced by the study of fraud—a fancy, labyrinthine topic that’s utterly fascinating.

The Story of My Seduction

In the summertime of 2001, I developed a workshop to administer the emotions of feedback, alongside an experienced leadership development program director, for 60,000 employees worldwide. Unfortunately, it was to not be. In lower than 1 12 months, this massive international organization of greater than 80,000 individuals would stop to exist. What happened in the midst of its collapse piqued my interest in fraud and white-collar crime.

The organization was Arthur Andersen. Starting in fall 2001, this almost 90-year-old giant accounting firm was exposed and enmeshed in a fraud perpetrated by Enron, an energy company based out of Houston, Texas. Enron was illegally hiding financial losses and withholding them from Andersen.3 Ultimately, Andersen lost its license to practice accounting—but more importantly, it lost its credibility as an audit firm when it was accused of shredding Enron’s audit workpapers.

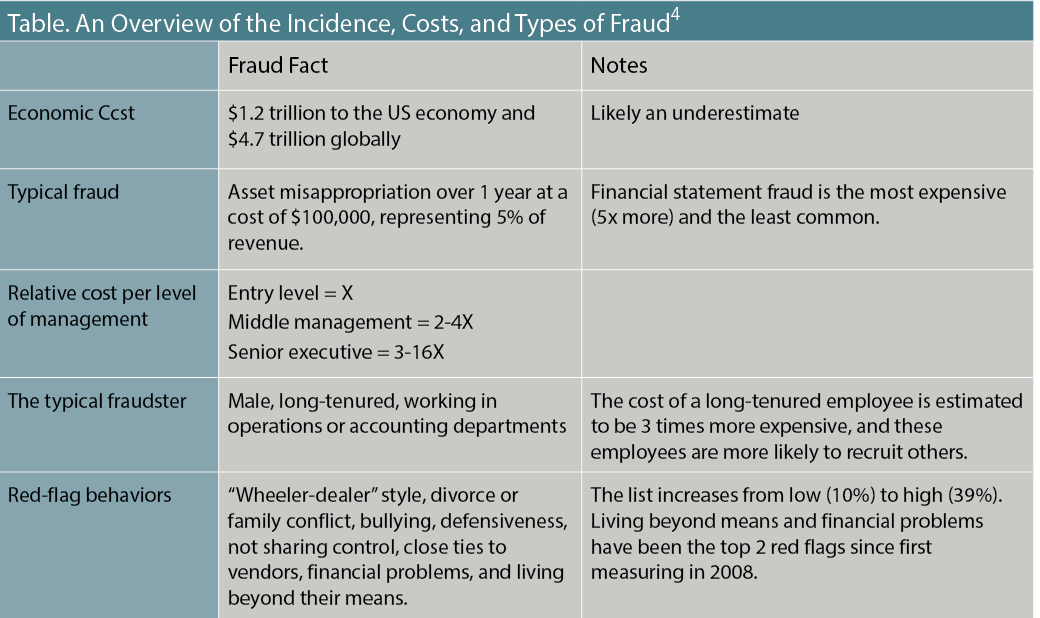

What Is Known of the Incidence and Forms of Fraud

From an organizational psychiatry perspective, fraud can have significant implications for the mental health of all who work inside organizations. Since 1996, the Association of Certified Fraud Examiners (ACFE) has released its biennial global survey of fraud, Report back to the Nations (RTTN). The Table shows summary data from the May 2022 RTTN.4

Table. An Overview of the Incidence, Costs, and Forms of Fraud4

As noted within the Table, the long-tenured worker is the most costly in terms of fraud. These individuals are best characterised as “wolves in sheep’s clothing.”5

Nevertheless, also of substantive interest are members of the C suite, particularly the chief executive officer (CEO) and the chief financial officer (CFO). As these individuals are the company leaders accountable for setting the tone from the highest and implementing internal controls inside the organization, the ACFE RTTN surveys identifies the CEO and the CFO as amongst the most costly in terms of fraud.4

Indeed, these highly placed individuals who occupy seats of power even have access to assets, in addition to the flexibility to override controls and risk management safeguards in place. These are the equivalent of “foxes guarding the henhouse.”

Leaders, especially those within the C suite, have to be held accountable for managing the individuals of their organizations and for creating sustainable value creation strategies, and organizations which might be fraud-resistant. Because these and other leaders oversee the execution of plans, are accountable for risk, and are visible to so many each inside and out of doors the organization, their mental health is critically vital.

Who Exactly Commits Fraud—and Why?

One of the steadily asked questions on fraud behavior is, “What’s the profile of the fraudster?” To deal with this query, I used to be invited by ACFE/University of West Virginia’s Institute for Fraud Prevention (IFP) to assemble a team to explore the human side of fraud within the early 2000s. Right now, I used to be a part of an interdisciplinary team assembled by my colleague and regular coauthor, Sridhar Ramamoorti, PhD, to explore the human side of fraud. He contributed significantly here, in truth.

Our multidisciplinary team sought to deal with fraud in latest ways on the IFP, especially the novel but welcome perspective of an organizational psychiatrist. Ultimately, we recognized that profiling had limited usefulness and was even a dead end. What was more vital was to know how and why fraud was committed.

Because fraudsters could be either short- or long-standing employees, and since in addition they work in groups, we began to deal with several latest questions related to fraud, including:

- What makes fraud victims at risk of fraudsters?

- Fraudsters often don’t see themselves as greedy—so, how do they see themselves?

- Because fraud is so expensive when perpetrated by senior executives, how can we understand fraud within the C suite higher?

- Does it make sense to see fraud as perpetrated by a single individual, or is it price our time to check fraud less like we’d a serial killer and more like gang behavior?

- Is profiling the correct solution for detecting fraudsters?

In dialogue with ACFE leadership and the IFP, we developed a taxonomy out of the concept of the “bad apple.” We began to have a look at not only the “bad apple,” or the fraudster, but additionally the “bad bushel” and “the bad crop.” This led to our paper,6 which in turn led to our book, A.B.C.’s of Behavioral Forensics.7

One problem became our focus: Why do these employees commit fraud? We found that employees who commit fraud often fall into 1 of two categories:

- The accidental or situational fraudster: the worker who thinks “the organization can afford this” or “it’s just money.” (These thoughts normally involve quite a few rationalizations.)

- The predatory fraudster: the worker with predatory intent who deliberately stalks their victims and may even create opportunities to commit fraud.5 (A lot of these predatory types have little or no conscience, and hence, don’t need any rationalizations.)

Selecting to interrupt the law, or the potential to achieve this, is one other subject of interest. In exploring this further, we found that reversal theory (RT), pioneered by psychologist Michael Apter, PhD, conceptualizes fraud behavior quite well by explaining that everybody breaks rules (the law), and it allows for motivational states to vary over time.8

As our colleague from law enforcement, Joe Koletar, DPA, CFE, notes, everyone breaks the law after they go 1 mile per hour over the speed limit. His point is that each one of us, despite being aware of the law, have the potential to decide on to interrupt the law.9

The RT model provides 2 further pertinent reasons8:

- There are more motivational states for investigators to explore related to “moving into the mind of the fraudster.” Considering “greed” as the first motivation to commit fraud blocks moderately than allows access into the human mind.

- These motivational states can change based on one’s sense of danger (ie, risk perception).

The RT model explains how individuals can take significant risk while ignoring the natural alarms. We achieve this through using a psychological “protective frame,” by which we feel insulated from dangerous situations if we’re capable of feel protected by physical or psychological distance from harm.8 This explains why we could be excited in a horror movie or within the presence of sharks in a shark cage.

Because it applies to fraud, this explains why the Enron energy traders, for example, could do the harm they did to the residents of California who went bankrupt—and even lost their homes in lots of cases—when they might not afford their electricity bills: These Enron traders, based in Houston, Texas, were far faraway from directly experiencing the psychological harm inflicted on these residents.

Similarly, Patrick Kuhse, who illicitly made $3.89 million when he was deputy bond trader for the state of Oklahoma within the early Nineteen Nineties, said he felt that individual residents of the state probably suffered very minor losses and relied on this “diffusion of harm” logic to argue that it was a victimless crime.10,11 This protective frame model generally explains the “victimless” rationale of those that commit fraud inside their very own organizations: These individuals literally don’t see the harm done to trust, to opportunity, and, after all, to the fame of the organization.

Clearly, in certain cases of predatory fraud (eg, phishing or other scams done intentionally through social manipulation), the fraudster knows the harm they’re causing. On this sense, their intentions are more pathological and fit that of a psychopath. This matches the behaviors of leaders who sell their very own stock while telling employees to retain theirs (eg, the late Ken Lay at Enron), and of those that overtly misinform investors, customers, and even patients.

As we explored motivations further, one other individual got here into focus: the victim. Our early models sought to spotlight the necessity to know this person, who is usually forgotten within the pursuit of “the fraudster” profile. In our book, A.B.C.’s of Behavioral Forensics, we used cases and customary experiences to explain the dynamic dance between the predator and the victim.7

Fraud involves violation of trust and due to this fact requires the cooperation of the victim. Nevertheless, it will be significant to know that fraud is just not a victimless crime. Employees suffer when the business underperforms in accidental fraud, and in predatory fraud, the crime requires the cooperation of the victim.

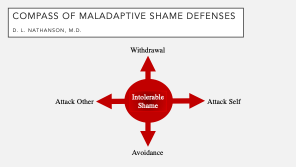

A Role for Psychiatry: Shame Incompetence

A crucial conceptual piece explains most of what we see in fraud comes all the way down to emotional incompetence and, specifically, shame incompetence (Figure 1).12

Figure 1. Compass of Maladaptive Shame Defenses12

On the skin, many high-profile fraudsters seem like shameless, or at the least not “shame-phobic.” A lot of these fraudsters pursued a larger-than-life and really public personae—but beneath the surface, there was far more happening. Some research suggests that these individuals may not have a healthy self-esteem. Current concerns have been voiced about an idealization of billionaires and other signs of wealth (eg, social media influencers), and our approach to behavioral forensics notes that the victims of C-suite fraud are lively within the fraud due to their adulation.

Within the case of Enron, when the organization was failing on the very end, the corporation’s leaders famously and charismatically addressed rooms filled with employees and encouraged them to carry onto their stock while, privately, they were selling their very own shares. Elizabeth Holmes, former CEO of Theranos, did the identical not only with Theranos employees, but additionally with investors and the US military.

These behaviors usually are not unlike those of authoritarian leaders as they reinforce their power and fulfill their capability for theft and abuse of the federal government—or, on this case, the organization.13

From a twinge of self-consciousness to profound humiliation, the effect of shame is instantly understood and seen within the fraud dynamic. It’s adaptive as we repair and reintegrate when the inevitable ruptures to relationships occur. It’s maladaptive when, as may often be the case with fraudsters, it moves our self-esteem further away from reality.

Listed here are examples of the predator’s lack of shame:

- “Why would they query my results? Don’t they see I work so hard? In truth, I never take a sick day and sometimes work holidays!” (This might be to hide the fraud that they’re committing.)

- “How can I show up on the country club, the CEO roundtable, or on the analysts’ call without numbers representing solid performance, as the corporate is me and I’m the corporate?” (“Fake it ‘til you make it” has been the motto of many a Silicon Valley CEO, including Elizabeth Holmes.)

- “I’ve worked so long for modest pay while others I do know have lived a superb life. The corporate makes enough money and hasn’t noticed me, so that they won’t notice this going to me. Besides, I pays it back.” (Any such self-justification allows them to sleep at night unperturbed.)

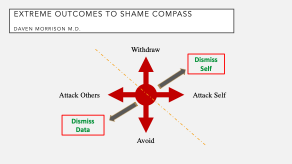

All of those are influenced by shame, and all are different motivations, per Apter’s RT model.8 To construct on this, we modified the shame compass to incorporate the acute outcomes that could be related to maladaptive shame defense: the dismissal of knowledge and the dismissal of self (Figure 2).7

Figure 2. Extreme Outcomes Associated With the Shame Compass7

In some cases, the self-dismissal of this modified shame compass resulted in suicide after the fraud was exposed. For instance, J. Clifford Baxter, former vice chairman of Enron, committed suicide within the wake of Enron’s fraud scandal.14 Ian Gibbons, chief scientist at Theranos, also committed suicide.15

As psychiatrists, we see maladaptive defenses day by day. In our patients, we see the distorted self-esteem of mania and dual diagnosis. We all know we could be “conned.” As professionals, we’ve got seen the overly confident peers who bully departments for more influence while those that are impaired with “imposter syndrome” never fully develop professionally. Nevertheless, although we all know this clinically and personally, most psychiatrists don’t have a model of emotions that helps. We’d like to make use of such a model to assist our patients and ourselves.

There’s a growing body of literature on members of the “dark triad” of personalities: narcissists, Machiavellians, and psychopaths/sociopaths.16 When in powerful corporate positions, all these individuals—who fall under the antisocial personality disorder classification within the DSM-5—have a tendency for committing fraud.

Epstein and Ramamoorti argue that, unlike individuals who require incentives or pressure, in addition to rationalization to justify any unethical, immoral, or illegal behaviors, individuals inside the “dark triad” of personalities—who’ve little or no conscience and low or non-existent empathy—only need opportunity to commit fraud.5 Psychiatrists can play a key role in higher understanding such abnormal personalities, learning how these individuals manipulate emotions, and learning how—and why—they decide to perpetrate fraud.

Concluding Thoughts

So, what’s the following frontier within the fight against white-collar crime—one by which psychiatrists can play a big role in the event that they select? When studying fraud further, we’d like to give attention to the behavior—not the person—and to start out seeing emotions as data. If we in psychiatry can higher understand who commits fraud and why, we could also be in a greater position to stop future instances of fraud, in addition to to assist those that are affected by fraud.

Dr Morrison is a clinical assistant professor of psychiatry at Rosalind Franklin University’s Chicago School of Medicine, and past president of the Academy of Organizational and Occupational Psychiatry. He can also be a member of the Group for the Advancement of Psychiatry (GAP)–Committee on Work & Organizations; Institute for Fraud Prevention (IFP); Tomkins Institute of Applied Studies of Motivation, Emotion and Cognition. He’s a co-author of A.B.C.’s of Behavioral Forensics and Psychiatry of Workplace Dysfunction, and an everyday contributor to the B4G™ blog, bringingfreudtofraud.com.

Dr Ramamoorti is currently an associate professor of accounting on the University of Dayton and the managing principal and CEO of The Behavioral Forensics Group™ LLC. He can also be an everyday contributor to the B4G™ blog, bringingfreudtofraud.com.

References

1. Sutton W. Where the Money Was: The Memoirs of a Bank Robber. The Viking Press; 1976.

2. Granelli JS. Con man on how to not be taken to cleaners: fraud: former ZZZZ Best whiz kid Barry Minkow, fresh from prison, tries to make amends on lecture circuit. The Los Angeles Times. October 13, 1995. Accessed November 5, 2022. https://www.latimes.com/archives/la-xpm-1995-10-13-fi-56692-story.html

3. The autumn of Andersen. Chicago Tribune. September 1, 2002. Accessed November 5, 2022. https://www.chicagotribune.com/news/chi-0209010315sep01-story.html

4. Occupational fraud 2022: a report back to the nations. Association of Certified Fraud Examiners. May 2022. Accessed November 5, 2022. https://legacy.acfe.com/report-to-the-nations/2022/

5. Ramamoorti S, Epstein BJ. Today’s fraud risk models lack personality: auditing with ‘dark triad’ individuals in the chief ranks. The CPA Journal. March 2016. Accessed November 5, 2022. https://www.cpajournal.com/2016/03/16/todays-fraud-risk-models-lack-personality/

6. Ramamoorti S, Morrison D. Bringing Freud to fraud: understanding the state-of-mind of the C-level suite/white collar offender through “A-B-C” evaluation. Accounting Faculty Publications. 2009;71.

7. Ramamoorti S, Morrison DE, Koletar JW, Pope KR. A.B.C.’s of Behavioral Forensics: Applying Psychology to Financial Fraud Prevention and Detection. Wiley; 2013.

8. Apter MJ. Reversal Theory: The Dynamics of Motivation, Emotion and Personality. Oneworld Publications; 2006.

9. Koletar J. All of us break the law. Bringing Freud to Fraud. March 10, 2015. Accessed November 5, 2022. https://bringingfreudtofraud.com/?p=358

10. Bodor J. Ex-broker details descent into crime. Telegram & Gazette. October 6, 2005. Accessed November 5, 2022. https://www.telegram.com/story/news/local/north/2005/10/06/ex-broker-details-descent-into/53171451007/

11. Mintchik N, Riley J. Rationalizing fraud: how considering like a crook might help prevent fraud. The CPA Journal. 2019. Accessed November 5, 2022. https://www.cpajournal.com/2019/04/15/rationalizing-fraud/

12. Nathanson DL. Shame and Pride: Affect, Sex, and the Birth of the Self. W W Norton & Co Inc; 1992.

13. Post JM. Leaders and Their Followers in a Dangerous World. Cornell University Press; 2004.

14. The Associated Press. Police say former Enron executive committed suicide. The Recent York Times. January 25, 2002. Accessed November 5, 2022. https://www.nytimes.com/2002/01/25/business/police-say-former-enron-executive-committed-suicide.html

15. Carreyrou J. Bad Blood: Secrets and Lies in a Silicon Valley Startup. Knopf; 2018.

16. Paulhus DL, Williams KM. The dark triad of personality: narcissism, Machiavellianism, and psychopathy. J Res Pers. 2002;36(6):556-563.